The global economy may be approaching another turning point. After two years of cooling inflation and hopes for monetary easing, 2026 could bring a renewed wave of price pressures. According to Sergey Perminov, Head of Analytical Support at the Treasury Department of Freedom Broker, global inflation risks are once again building beneath the surface, DKNews.kz reports.

In his view, the U.S. economy is currently overstimulated.

“The U.S. economy has been excessively supported: the fiscal deficit is enormous, while the Federal Reserve maintains a relatively soft stance despite elevated inflation and historically low unemployment,” says Perminov.

The U.S.: An Overheating Economy?

According to the Bloomberg consensus forecast, the U.S. federal budget deficit is expected to increase from 6 percent to 6.4 percent of GDP in 2026. This is an unusually high level outside of wartime or major crises.

At the same time, inflation in the U.S. has exceeded its target level for five consecutive years. Yet markets expect the Federal Reserve to cut rates by approximately 50 basis points this year.

Perminov argues that the Fed responded too slowly to the post-pandemic inflation surge, and may now be easing too quickly.

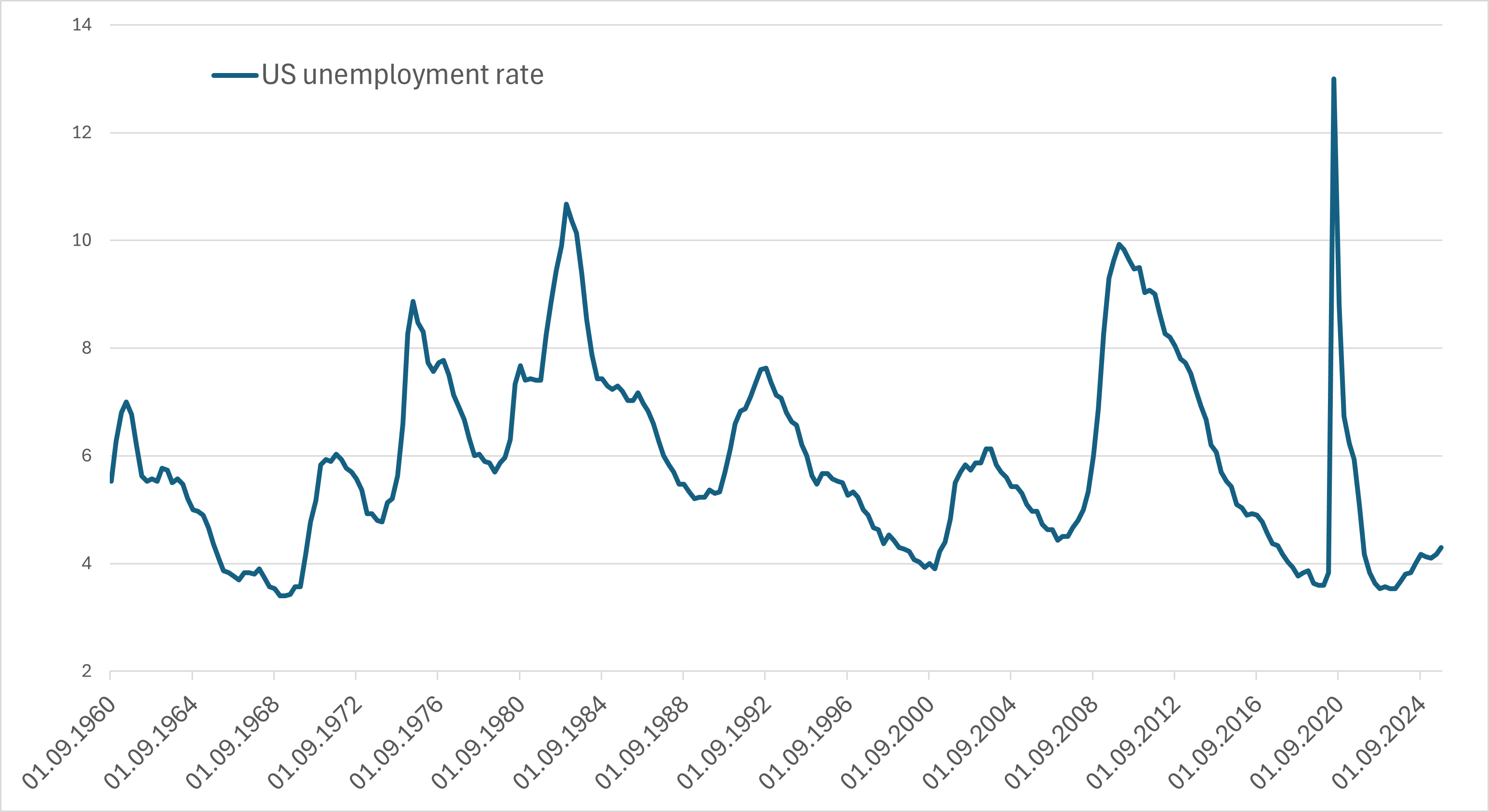

“The Fed’s reaction function appears to have become structurally more dovish: priority is increasingly given to the labor market rather than inflation. This is happening with unemployment at around 4.3 percent, close to historical lows,” he notes.

Tighter immigration policies further constrain labor supply, keeping the job market tight even amid economic slowdown. This dynamic may sustain inflationary pressure rather than ease it.

Artificial Intelligence: A New Source of Inflationary Pressure?

Another key driver in 2026 could be the investment cycle in artificial intelligence.

According to Dealogic data cited by Reuters, U.S. technology companies raised $342 billion in debt in 2025 to finance AI investments. This was a record figure and may persist into the coming year.

“Previously, many major tech companies had negative net debt. Today they are not only investing all their earnings but also increasing leverage to avoid losing the race for AI leadership,” Perminov explains.

Given the scale of the technology sector, this structural shift carries macroeconomic implications. Massive AI investments could create bottlenecks in supply chains, energy infrastructure and related industries. Large tech companies are capable of paying almost any price for critical resources, intensifying price pressures.

Even if AI-related stocks correct in 2026, Perminov believes the deflationary effect of a market downturn would likely not offset the short-term inflationary impact of real capital expenditures.

A New Bull Market in Commodities

Another important theme for 2026 is the expansion of the commodities bull market.

The sharp rise in gold prices in 2024-2025 has begun lifting other metals. Silver has broken through multi-year resistance levels, while copper has delivered its strongest performance since 2009 - a classic signal of a reflationary phase.

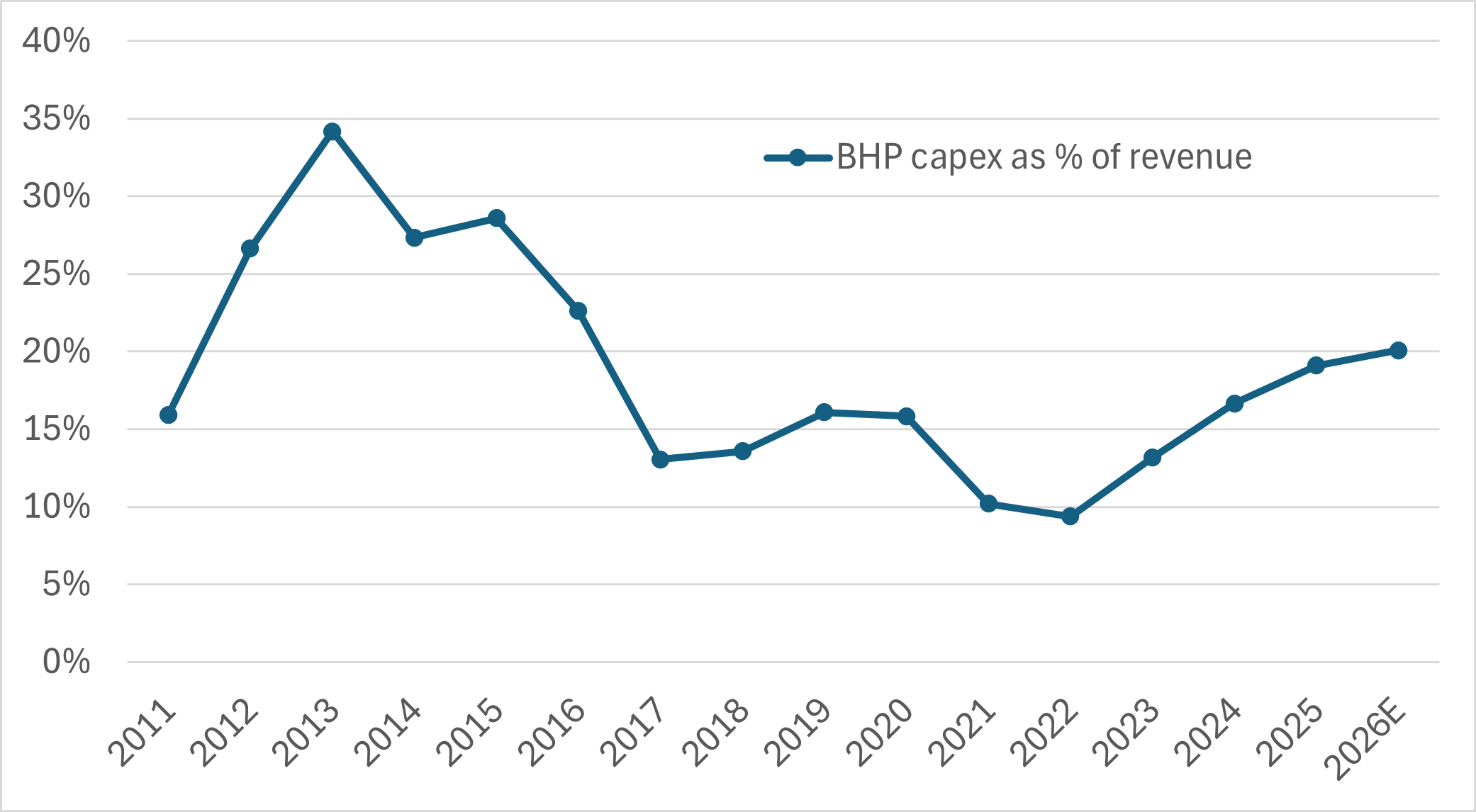

At the same time, supply growth remains constrained. Investment in resource extraction has been insufficient for over a decade. After the 2015-2016 commodity downturn, major mining companies sharply reduced capital expenditures and have yet to fully restore them.

Oil markets are also in focus. According to Perminov, underinvestment in the oil sector is even more pronounced than in metals.

“With virtually zero global spare capacity, any significant supply disruption could only be offset by demand destruction. That would require oil prices well above $100 per barrel,” he warns.

Interestingly, market sentiment toward oil remains pessimistic, even though energy stocks outperformed crude itself in 2025 - potentially signaling stronger long-term expectations.

Bond Yields and a Structural Shift

The rise in government bond yields in 2021-2022 may not have been a temporary post-pandemic effect, but rather the beginning of a long-term structural trend.

Chronic fiscal deficits in developed economies are becoming the new normal. This may mark a reversal of the decades-long era of falling yields and depressed commodity prices.

Switzerland, one of the few developed countries without a budget deficit and with a floating currency, has already seen rates return close to zero. Meanwhile, Japan, burdened by the largest public debt among advanced economies, is increasingly viewed as a risk source for long-duration bonds.

What This Means for Investors

According to Perminov, the current environment may favor positioning toward higher yields, relatively inexpensive commodities (excluding precious metals) and shares of commodity producers.

Such assets can serve as an effective hedge not only against inflation but also against stagflation. If the U.S. economy overheats in 2026, a slowdown combined with persistent inflation could emerge in 2027.

For comparison, the combined market capitalization of Exxon Mobil and BHP is less than $800 billion - modest compared to the multi-trillion-dollar valuations of leading technology giants.

Don’t Be Misled by Temporary Calm

Inflation in early 2026 may appear subdued due to technical distortions related to the recent U.S. government shutdown. Bloomberg Intelligence estimates that these statistical effects may dissipate by April.

However, markets tend to look beyond short-term noise and focus on structural trends.

If the underlying drivers remain in place, 2026 could mark the true return of global inflation - and a fundamental shift in how investors assess risk, growth and asset allocation.