Central Asia is increasingly reshaping the global aviation map. Once seen mainly as the space between Europe and China, the region is now turning into an aviation corridor in its own right - with growing cargo flows, new routes and Kazakhstan’s strengthening role. IATA data shows that the country has already become the region’s main aviation gateway. But the next challenge is much more difficult - turning transit into a full-fledged economy, DKNews.kz reports.

Global aviation is not changing only in major airports such as Dubai, Istanbul, Hong Kong or Frankfurt. Sometimes new routes emerge in places that were once seen merely as “flyover territory.” Today, that story is unfolding in Central Asia.

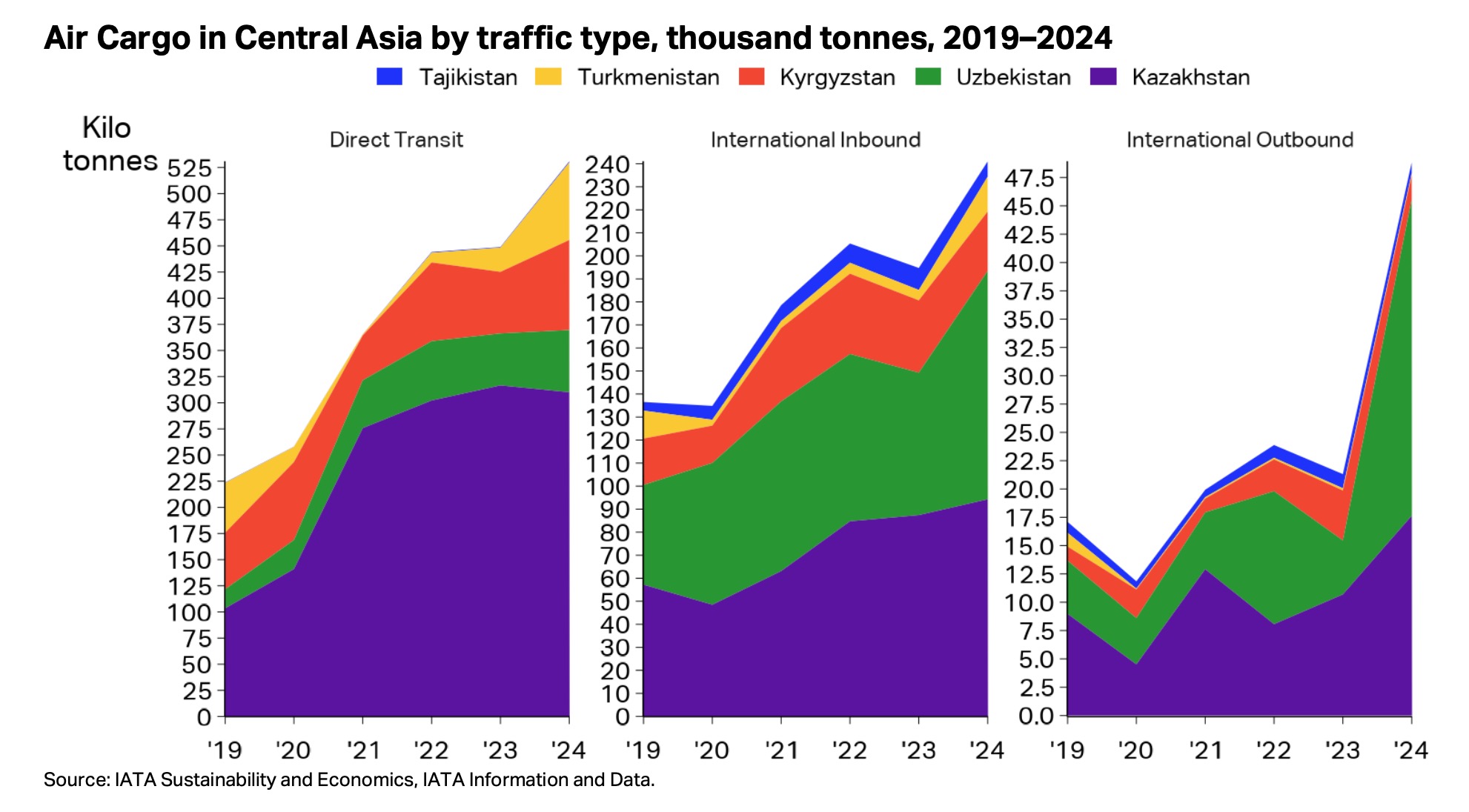

According to IATA data, the region is gradually becoming an intercontinental bridge for global cargo flows. Since 2019, air cargo volumes in Central Asia have more than doubled. Against the backdrop of stable volumes in Hong Kong and a decline in Frankfurt, this looks especially significant: a region that was once barely visible on the global map is now rapidly gaining weight.

And most importantly, Kazakhstan is at the center of this story.

From transit to a new role

Central Asia’s growth is largely linked to direct transit. It resembles the Anchorage model - when an airport becomes an important technical stop between major markets. Aircraft land, routes are reshaped, and geography suddenly turns into a competitive advantage.

For Kazakhstan, this is especially important. The country is located between Europe and Asia, close to major markets and new logistics corridors. When airspace is restricted, routes become longer and airlines search for more efficient solutions, Kazakhstan gets a chance to become not just a point on the map, but part of a new aviation architecture.

IATA states this clearly: Kazakhstan has strengthened its position as Central Asia’s main gateway. The country’s total cargo volumes in 2024 rose by 149 percent compared with 2019.

This is no longer just statistics. It is a signal that the global cargo market is beginning to look at the region differently.

But transit is only the first layer

There is an important nuance. Transit alone does not always bring a major effect for the local economy. If an aircraft simply lands, refuels and departs, the country receives part of the operating income, but does not create a full logistics chain.

Real value appears when transit turns into cargo handling, consolidation, warehousing, service, maintenance, digital logistics, customs efficiency and new jobs.

This is where IATA data gives an interesting signal: in Central Asia, not only direct transit stops are growing, but also inbound, outbound and connecting flows. The sharp rise in outbound volumes in 2024 is especially notable. It may suggest that the region is moving beyond the simple role of a “technical stop” and is gradually becoming an active link between Europe and China.

For Kazakhstan, this is a decisive moment. Being a transit territory is useful. But being a logistics center is far more valuable.

Kazakhstan’s aviation network has expanded, but remains vulnerable

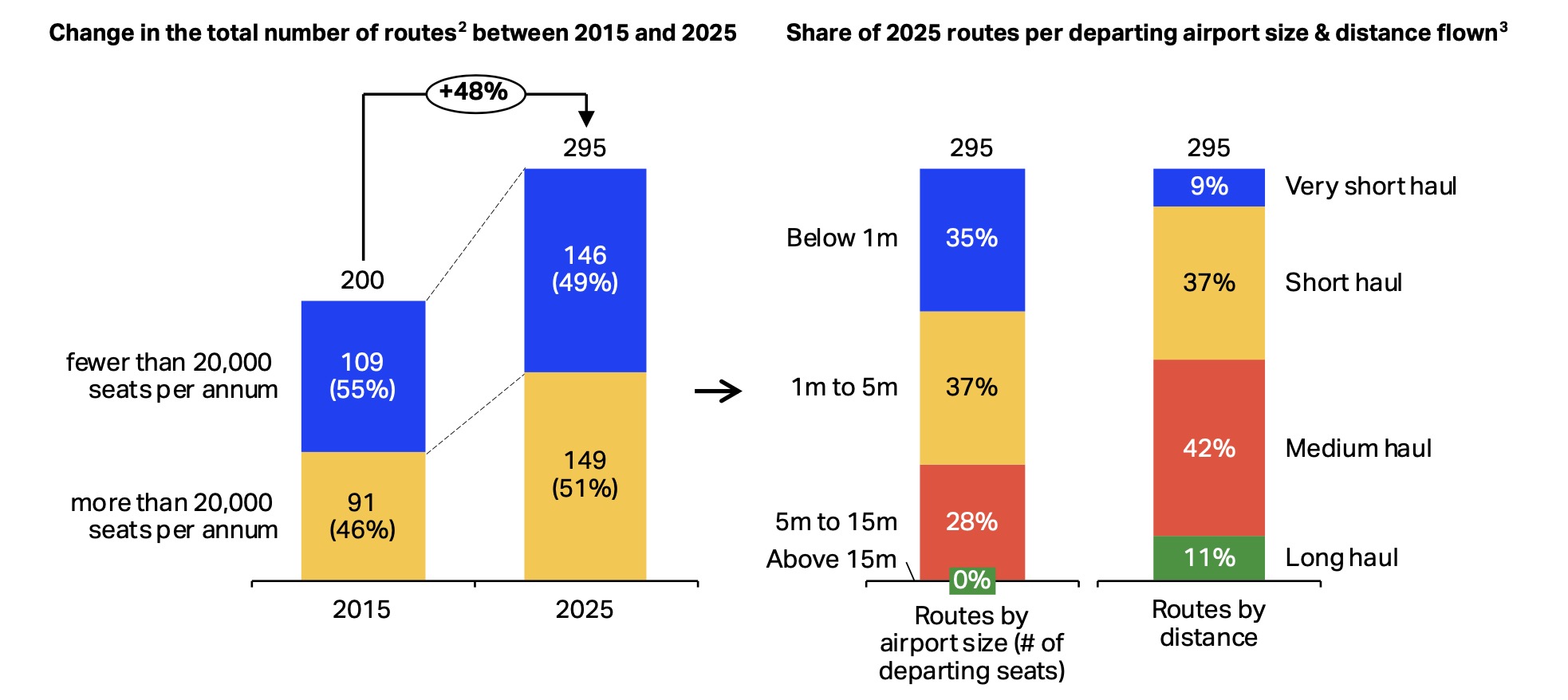

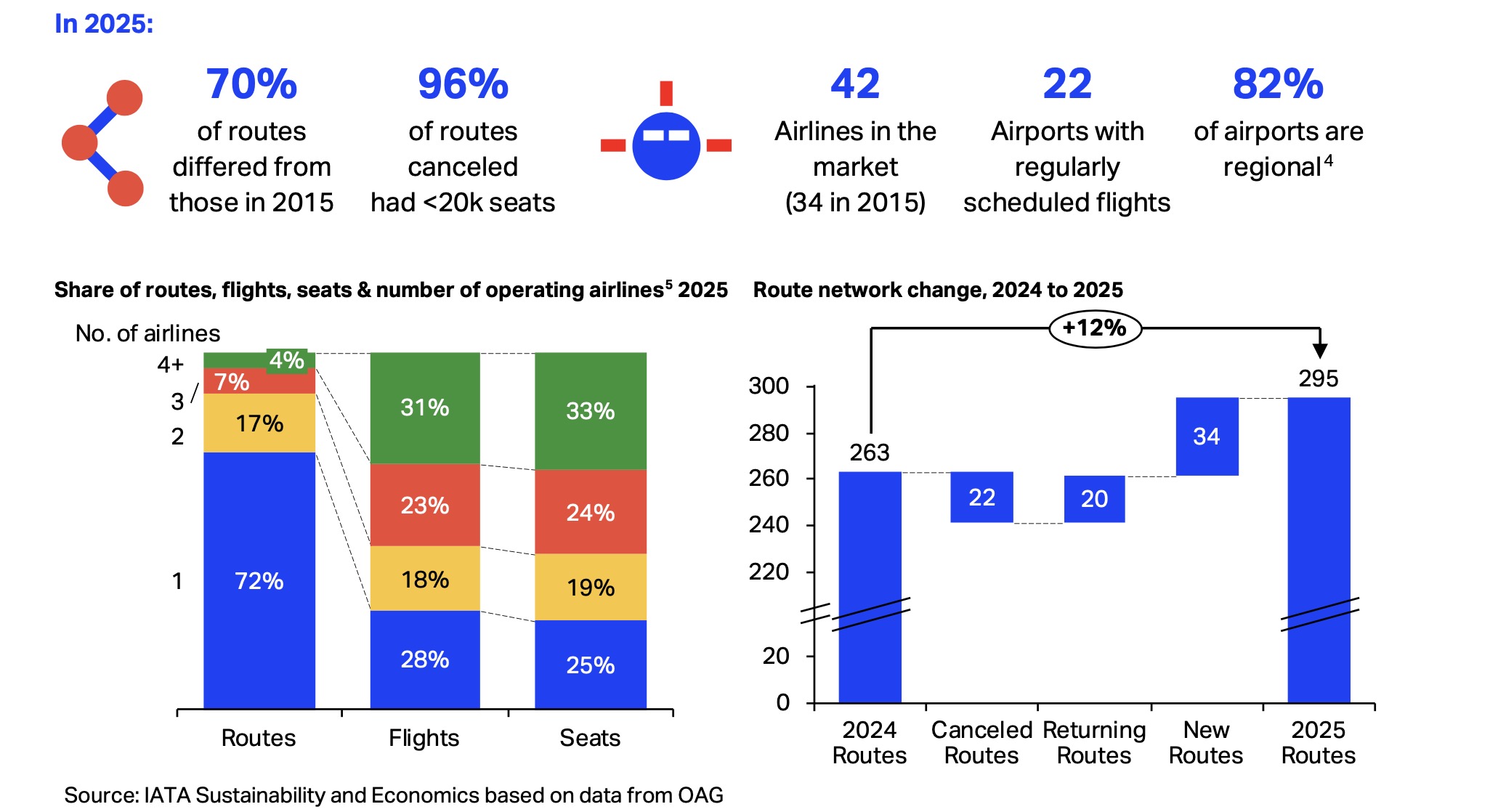

Alongside the cargo story, the country’s passenger map is also changing. According to IATA, Kazakhstan had 295 regular commercial routes in 2025. For comparison, there were 200 in 2015. That is growth of 48 percent.

At first glance, this is a strong result. More routes mean more mobility, more competition and more opportunities for regions.

But behind the attractive figure lies an important detail: nearly half of the routes in 2025 offered fewer than 20,000 seats per year. These are low-volume routes, and they are especially sensitive to external shocks - fuel prices, exchange rates, seasonality, paying demand and operating costs.

These are precisely the routes most often at risk of cancellation. IATA shows that 96 percent of the routes canceled in Kazakhstan were in the category of fewer than 20,000 seats per year.

In simple terms, regional aviation is growing, but it remains fragile.

Why this matters for ordinary people

For passengers, air connectivity is not abstract statistics. It is the ability to quickly get from a region to the capital, travel for medical treatment, education, work, an international connection - or simply avoid spending an entire day on the road.

For Kazakhstan, with its vast territory, the airplane is often not a luxury, but a tool for normal life. This is especially true for remote cities and regions.

IATA separately notes that regional air links often provide critical lifelines for remote communities, while at the same time being among the most vulnerable to external economic pressures.

This is a very Kazakh story. The country has 22 airports with regular scheduled flights, and 82 percent of them are regional. In other words, aviation development is not only about Almaty and Astana. It is about the entire map of the country.

There is competition, but not everywhere

Another important figure: in 2025, 42 airlines operated in Kazakhstan’s market, compared with 34 in 2015. This is a positive sign of market openness and growing interest in the country.

However, competition is not distributed evenly. According to IATA, 72 percent of routes are served by only one airline. These routes account for 28 percent of flights and 25 percent of available seats.

For passengers, this means a simple thing: in some places, the choice of carriers is expanding, while in others it remains almost nonexistent. If a route is served by only one airline, any change in that carrier’s schedule, fleet or economics can immediately affect the accessibility of the destination.

That is why the resilience of an aviation network depends not only on the number of routes on paper. What matters is how frequent, stable, competitive and economically viable they are.

The route map is changing faster than it seems

Another IATA figure sounds almost like a warning: 70 percent of Kazakhstan’s routes in 2025 differed from those in 2015.

This shows how quickly the aviation network is changing. Some routes disappear, others return, and new ones appear for the first time. Between 2024 and 2025 alone, the number of routes increased from 263 to 295. In one year, 22 routes were canceled, 20 returned and 34 new routes were launched.

This is a living market. But a living market does not always mean a stable one.

For the state, airports and airlines, this requires careful calibration: which routes need support, where there is demand, where frequency is lacking, where regional services should be developed, and where international potential should be unlocked.

Kazakhstan can benefit from the new aviation map

The main conclusion from IATA data is simple: Kazakhstan is in the right place at the right time. The world is rebuilding routes, cargo is looking for new corridors, Central Asia is growing, and the country already has the basic infrastructure, market and geography to strengthen its role.

But from here, everything depends on the quality of decisions.

If Kazakhstan limits itself to transit stops, the effect will be visible but limited. If it develops cargo hubs, customs services, multimodal logistics, regional airports, digital processes and a reliable passenger network, the country can gain far more.

Today, aviation is not only about aircraft. It is the economy of time. Whoever connects cities, markets and people faster gains an advantage.

Central Asia is already appearing on the new map of global air cargo. On this map, Kazakhstan looks like the main entrance to the region. The question now is different: can the country turn its favorable geography into long-term aviation strength?

Because transit is an opportunity. A hub is a strategy.