Eurasian Economies to Grow by up to 9.3% in 2026

The Eurasian Development Bank (EDB) has presented its Macroeconomic Outlook for 2026–2028, DKNews.kz reports.

According to EDB analysts, investment activity and domestic demand will remain the key drivers of growth in most countries of the region, despite moderate global economic expansion and persistently elevated interest rates.

Key takeaways:

- The region’s GDP is projected to expand by 2.3% in 2026, with the Kyrgyz Republic (9.3%), Tajikistan (8.1%), Uzbekistan (6.8%) and Kazakhstan (5.5%) remaining the growth leaders.

- Inflation will continue to slow down to 6.3% in 2026, supported by prudent monetary policy.

- Investment remains the key driver of growth in the region, particularly in manufacturing, mining, energy and construction.

- Commodity markets are expected to show divergent trends: oil prices will decline slightly, while metal and gold prices will remain elevated.

- The US dollar is gradually losing its share in central bank reserves, while its role in settlements remains stable.

More about the report:

The EDB’s Macroeconomic Outlook presents a preliminary overview of economic developments in the Bank’s member states for 2025, along with key macroeconomic projections for 2026 as well as for 2027 and 2028.

EDB analysts expect aggregate GDP growth across the seven member states to reach 2.3% in 2026, with most countries maintaining high levels of economic activity. In 2026, GDP growth is projected at 5.3% in Armenia, 1.8% in Belarus, 5.5% in Kazakhstan, 9.3% in the Kyrgyz Republic, 1.4% in Russia, 8.1% in Tajikistan and 6.8% in Uzbekistan.

World Economy

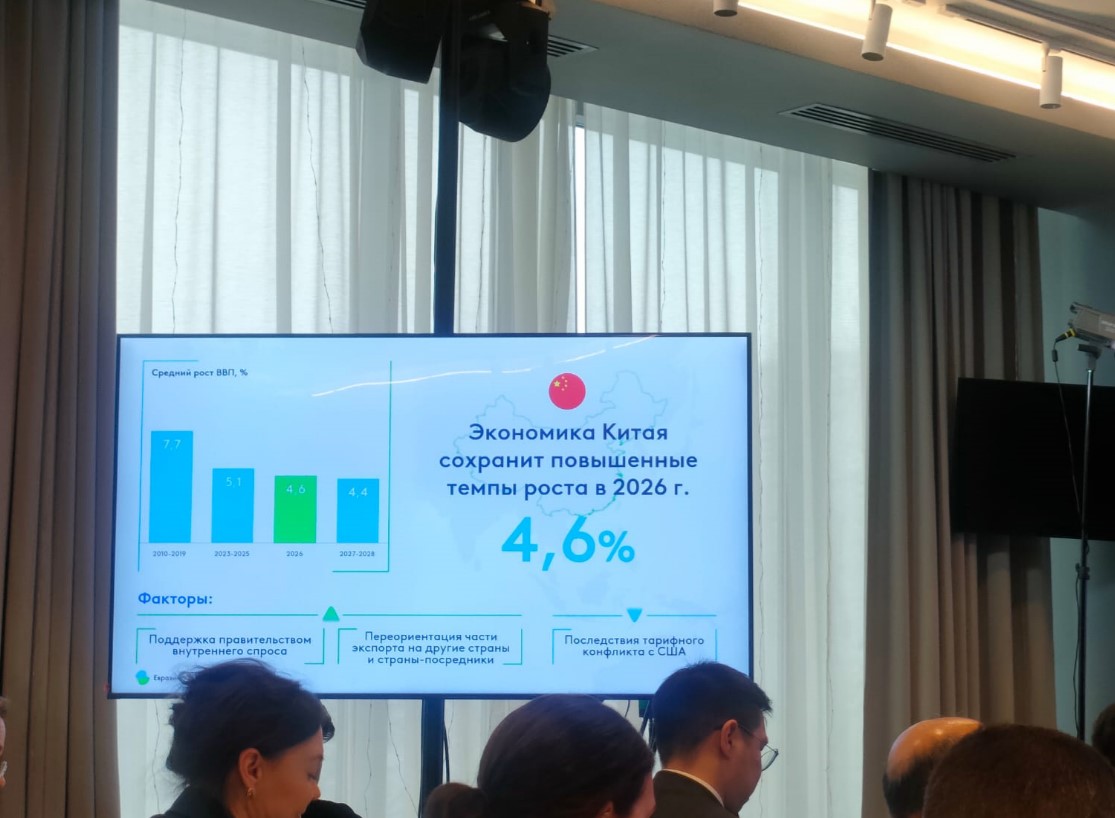

According to EDB analysts, the global economy will grow at a slightly slower pace than in 2024–2025 and will gradually adapt to new trade restrictions. In the US, 2026 is expected to record GDP growth of around 1.6% amid tariff-related conflicts and high debt levels. The eurozone economy is projected to expand by 1.1%, mainly due to increased government spending on defence and infrastructure. China will remain a growth driver, with a forecast of 4.6% in 2026, supported by government measures to stimulate domestic demand.

Inflation in the US and the eurozone is expected to remain above target levels in 2026–2028, while interest rate dynamics will diverge. In the US, rate cuts are likely to proceed slowly due to rising costs associated with tariff conflicts. According to EDB analysts, the ECB completed its rate-cutting cycle in 2025 and will begin gradually raising rates in 2026–2027.

The Macroeconomic Outlook notes that after a period of low interest rates in the 2010s, global economies have returned to a higher, “normal” level of rates typical of the period preceding the era of ultra-cheap money. This shift creates additional risks for financial stability and investment, as both companies and governments need to refinance substantial volumes of debt. As a result, interest rates will constrain global economic growth through higher interest payments and reduced availability of investment financing. This issue is examined in greater detail in Box 1 of the Macroeconomic Outlook.

In 2025–2027, commodity markets are expected to exhibit mixed trends. Oil prices are forecast to decline slightly due to increased supply, while metal prices will rise amid increasing infrastructure projects and the development of green energy. Gold prices are anticipated to remain high, driven by stronger demand for the metal as a reserve asset against the backdrop of geopolitical instability and the de-dollarisation trend.

In Box 2 of the Macroeconomic Outlook, EDB analysts examine changes in the role of the US dollar in the global economy. They conclude that the dollar’s share in central bank reserves is gradually and steadily declining, while its use in international settlements continues to increase and its role in credit and deposit operations remains stable.

Eurasia

Projected global economic and commodity market trends are not expected to create significant obstacles to economic growth in the Eurasian region, but nor are they likely to become a growth driver.

Lower oil prices will constrain export revenues for energy-exporting countries such as Kazakhstan and Russia, but are not expected to exert substantial pressure on their economic growth. For net oil-importing countries, including Armenia, Belarus, the Kyrgyz Republic, Tajikistan and Uzbekistan, lower prices will improve terms of trade and help restrain domestic price growth. Elevated gold prices will boost foreign exchange earnings for regional exporters such as the Kyrgyz Republic, Tajikistan and Uzbekistan.

In 2025, the EDB region of operations is returning to a moderate equilibrium growth trajectory following two years of record expansion. According to EDB analysts, regional GDP growth will slow to 1.9% by the end of 2025, compared with 4.5% in 2024, primarily due to a cooling of the Russian economy. At the same time, several Central Asian countries are expected to demonstrate record-high growth rates by the end of 2025, enabling them to maintain their external debt at a stable level despite the active capital raising. This enhances their investment attractiveness relative to other developing economies where debt burdens have risen sharply.

In 2026, the region’s economy is expected to continue expanding at a steady pace of 2.3%. In most countries, growth will remain robust, driven by strong investment activity. Inflation will gradually decline towards target levels, with regional price growth slowing to 6.3% in 2026 from 6.9% in 2025, assuming no additional shocks and reflecting prudent monetary policies pursued by regulators in EDB member states.

Key macroeconomic projections for EDB member states in 2026

Source: EDB analysts’ calculations.

Armenia

According to EDB forecasts, Armenia’s economic growth will remain high at 5.3%. The main drivers will continue to be domestic consumer and investment demand, supported by a high level of savings and expanding lending. Inflation is expected to stabilise around the target range of 3±1% and reach 3.3% by the end of 2026. The average annual exchange rate of the dram is projected at 393 per US dollar due to growing imports amid high domestic demand.

Belarus

In Belarus, GDP growth is projected to remain at 1.8% in 2026, followed by acceleration in subsequent years. One of the main constraints will be weaker demand for Belarusian products due to an economic slowdown in Russia, Belarus’s key trading partner. At the same time, high investment and consumer activity will support economic growth. Inflation is expected to remain close to the updated target of 7%, with a faster slowdown constrained by imported inflationary pressures from Russia and labour shortages. The average exchange rate of the Belarusian rouble in 2026 is projected at 3.32 per US dollar. Moderate depreciation is associated with rising imports and declining goods exports amid continued net foreign currency sales by households, which support the exchange rate.

Kazakhstan

EDB analysts expect Kazakhstan’s economy to maintain steady growth of 5.5% in 2026. The implementation of the National Infrastructure Plan and the launch of the state programme ‘Order for Investment’ will mitigate the negative impact of lower oil prices. Economic growth will also be supported by an expansion of non-resource exports. Inflation is expected to decline after peaking in early 2026 due to the VAT increase. Moderately tight monetary conditions will help reduce inflation to 9.7% by the end of 2026. According to EDB forecasts, the average exchange rate of the tenge will be 535 tenge per US dollar in 2026, supported by a high base rate and growth in non-resource exports.

Kyrgyz Republic

In 2026, the Kyrgyz Republic is expected to remain the regional leader in terms of GDP growth, at around 9.3%. This growth will be driven by increased investment in transport, energy and water supply infrastructure, as well as housing construction. EDB analysts forecast inflation to slow to 8.3% by the end of 2026. A faster decline in inflation will restrain increases in tariffs and excise duties. The average exchange rate of the som in 2026 is projected at 89.2 per US dollar, supported by rising remittances and high gold prices, with gold remaining the country’s key export commodity.

Russia

In Russia, GDP growth is projected at 1.4% in 2026, followed by a return to sustainable growth rates, supported by continued fiscal stimulus and a recovery in lending. Inflation is expected to continue declining towards the target level and reach 5.5% by the end of 2026. The VAT increase and labour shortages will keep inflation above target. EDB analysts forecast that the rouble will weaken to around 97 per US dollar by the end of 2026, reflecting lower oil prices, gradual rate cuts and a reduction in foreign currency sales by the Bank of Russia.

Tajikistan

Tajikistan’s economy is expected to maintain high GDP growth of around 8.1% in 2026. The main growth drivers will be expanded capacity in energy and manufacturing, as well as higher prices for gold and non-ferrous metals. Inflation is projected to rise to 4.5% YoY by the end of 2026 and remain within the target range of 5±2%. The somoni exchange rate is expected to remain stable, supported by rising exports and remittances. According to EDB forecasts, the average exchange rate in 2026 will be approximately 9.8 per US dollar.

Uzbekistan

EDB analysts expect Uzbekistan’s economy to continue growing at a sustainably high rate of around 6.8% in 2026. Growth will be driven by strong investment activity and favourable gold prices. Inflation is anticipated to continue declining towards the Central Bank’s target and may slow to 6.7% by the end of 2026, supported by relatively tight monetary conditions and exchange rate stability, with the soum projected to average around 12,800 per US dollar over the year. The national currency will be supported by high remittance inflows and rising metal exports amid a favourable price environment.

The EDB’s Forecast. Key macroeconomic indicators of EDB member states (baseline scenario)

|

Indicator |

2024 |

2025 F |

2026 F |

2027 F |

2028 F |

|

|

Republic of Armenia |

||||||

|

GDP in constant prices, % |

5.9 |

6.0 |

5.3 |

5.3 |

5.1 |

|

|

Inflation (at the end of the period), % YoY |

1.5 |

3.3 |

3.3 |

3.3 |

3.0 |

|

|

Refinancing rate (annual average), % |

8.0 |

6.8 |

6.5 |

6.0 |

6.0 |

|

|

AMD/USD exchange rate (annual average) |

392 |

389 |

393 |

400 |

403 |

|

|

Republic of Belarus |

||||||

|

GDP in constant prices, % |

4.0 |

1.8 |

1.8 |

1.9 |

2.0 |

|

|

Inflation (at the end of the period), % YoY |

5.2 |

7.1 |

6.9 |

6.7 |

6.5 |

|

|

Refinancing rate (annual average), % |

9.5 |

9.7 |

9.75 |

9.75 |

9.75 |

|

|

BYN/USD exchange rate (annual average) |

3.25 |

3.08 |

3.32 |

3.66 |

3.89 |

|

|

Republic of Kazakhstan |

||||||

|

GDP in constant prices, % |

5.0 |

5.9 |

5.5 |

5.5 |

5.5 |

|

|

Inflation (at the end of the period), % YoY |

8.6 |

12.3 |

9.7 |

6.4 |

5.0 |

|

|

Base rate (annual average), % |

14.7 |

16.7 |

16.3 |

12.4 |

10.2 |

|

|

KZT/USD exchange rate (annual average) |

469 |

525 |

535 |

559 |

578 |

|

|

Kyrgyz Republic |

||||||

|

GDP in constant prices, % |

9.0 |

10.3 |

9.3 |

7.6 |

7.5 |

|

|

Inflation (at the end of the period), % YoY |

6.3 |

9.1 |

8.3 |

7.4 |

6.2 |

|

|

Policy rate (annual average), % |

10.5 |

9.2 |

11.0 |

11.0 |

11.0 |

|

|

KGS/USD exchange rate (annual average) |

87.1 |

87.4 |

89.2 |

91.9 |

93.3 |

|

|

Russian Federation |

||||||

|

GDP in constant prices, % |

4.3 |

1.0 |

1.4 |

2.0 |

2.1 |

|

|

Inflation (at the end of the period), % YoY |

9.5 |

6.0 |

5.5 |

5.1 |

4.5 |

|

|

Key rate (annual average), % |

17.5 |

19.2 |

14.4 |

12.2 |

10.5 |

|

|

RUB/USD exchange rate (annual average) |

92.4 |

85 |

94 |

104 |

109 |

|

|

Republic of Tajikistan |

||||||

|

GDP in constant prices, % |

8.4 |

8.3 |

8.1 |

7.2 |

7.1 |

|

|

Inflation (at the end of the period), % YoY |

3.6 |

3.0 |

4.5 |

4.7 |

4.9 |

|

|

Refinancing rate (annual average), % |

9.3 |

8.2 |

7.6 |

8.4 |

8.4 |

|

|

TJS/USD exchange rate (annual average) |

10.8 |

10.3 |

9.8 |

10.3 |

10.8 |

|

|

Republic of Uzbekistan |

||||||

|

GDP in constant prices |

6.5 |

7.4 |

6.8 |

6.4 |

6.3 |

|

|

Inflation (at the end of the period) |

9.8 |

7.5 |

6.7 |

5.8 |

5.2 |

|

|

Base rate (annual average),% |

13.8 |

13.9 |

13.7 |

12.4 |

11.6 |

|

|

UZS/USD exchange rate (annual average) |

12,652 |

12,647 |

12,800 |

14,100 |

15,100 |

|

|

Note: “F” – forecast; GDP and inflation are provided in % YoY; exchange rate to U.S. dollar — number of national currency units to 1 U.S. dollar. |

||||||

|

Sources: national agencies of EDB member states, EDB analysts’ calculations. |

||||||